Last week, I was speaking to a group of Startup founders that have gotten together to build a product. Now, this product isn’t necessarily a bad idea at first glance. I’m not going to go into detail about the product purely out of curtsy to the team, but of course the reason we met up was because the team felt confident that they had something of substance and that they were willing to raise and wanted me to have first dibs.

They were an ambitious bunch, with pitch decks talking about how they’re going to be a Unicorn. Of course, they had a slide dedicated to market capitalization of the competitors (truly globally large players indexing on listed markets from New York to Hong Kong). They claimed to have features that the competitors didn’t, they were “playing a different angle”.

Welcome to the world of Unicorns and Vapourware

The team of people that I had met didn’t really have a product. It was really more of a concept that could technically be achieved, vaporware for short.

Products that are pre-revenue, pre-development and in the “concept” stage.

I don’t really have anything against concepts, they were asking for a serious amount of money to get the project off the ground. Enough to hire a team of 10-ish, pay above market rates and cover costs for the first 12 months. What struck me was the fact that they’ve valued their concept significantly higher than the value of the business I’ve founded. We’re talking near 8 figures at pre-product.

Now I understand that you need capital to start off, but the logic they had to justify the valuation was the fact that they were only willing to let go of 5% of their business.

Why: They plan on doing multiple rounds of raises every year at significantly higher valuations.

Pitch to me: “You can exit in the next raise easily, we’re looking at becoming a Unicorn”

In the world of tech-startups, Unicorns aren’t something new. We call a business a Unicorn once they reach that elusive 9 figure valuation. Valuation is a whole other can of worms, but I’ll leave this video of Mark Suster’s talk at Stanford which is honestly just a breath of fresh air.

Where is the Alpha?

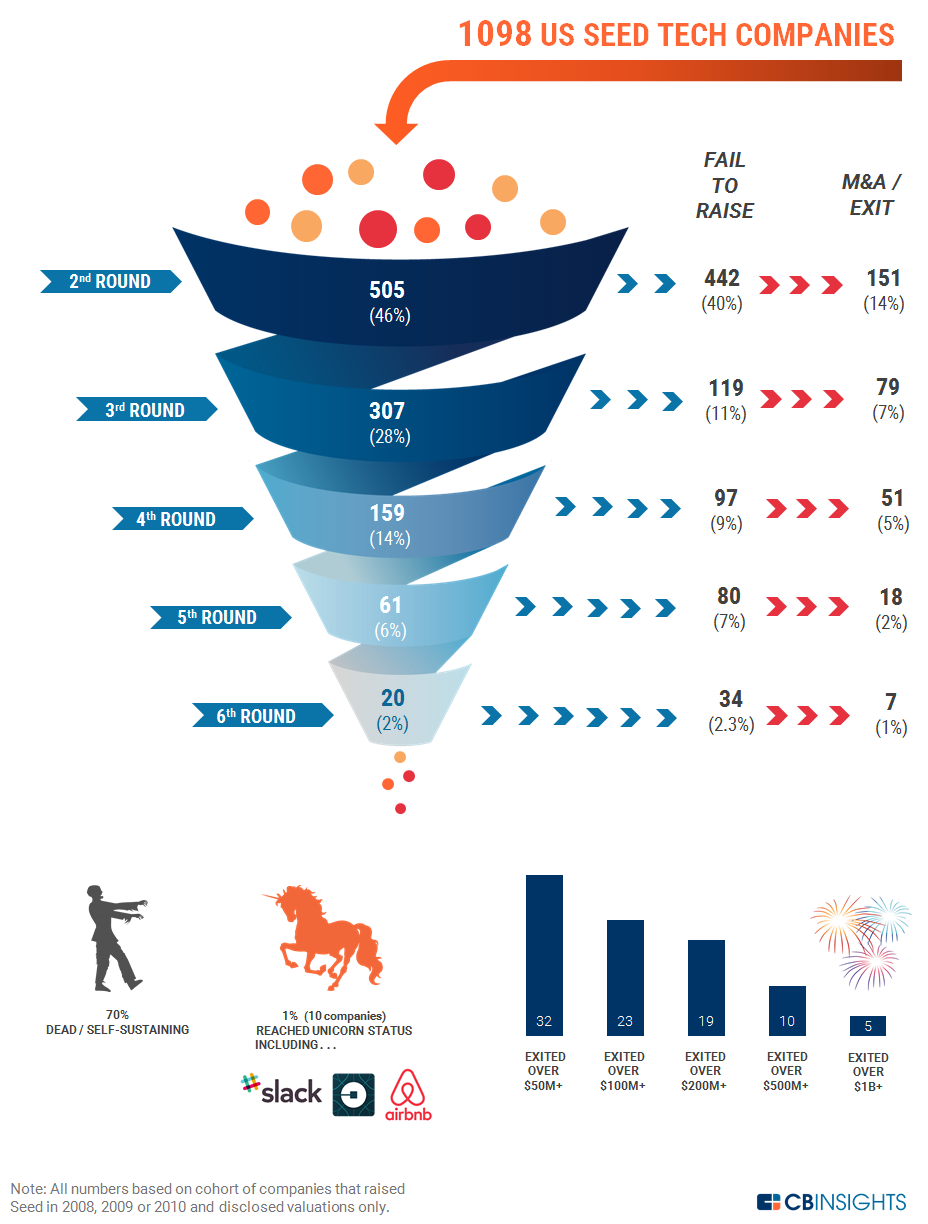

According to CB Insights, less than 1% of funded startups stand a chance of becoming a Unicorn in the current US landscape, significantly lower global average.

Backing startups are tricky, the way value chains work in a free market are quite simple. The person who generates the most value should always be the customer, the person buying a product or service. It then moves to an employee, the people making the product or service. Followed by the Management, Leadership and then finally Shareholders from seed stage investors to public markets.

If your startup raises at multi-million dollar valuations, burns through cash like a hot knife through butter on crazy office fit-outs, your full time cat-sitter and masseuse (or masseuse who also is a cat, win?) you’re going to have to add a shit ton of value into this world to make up and show a single cent back to an investor.

I follow a lot of investors and techies and listen to what they have to say to pass the time, one guy in particular I adore is Chamath Palihapitya form Social Capital. There’s probably a bias here because he’s probably one of the few Sri Lankan VCs/Startup guys that has actually “made it”. During the recent years, his life kind of almost fell apart, but everything he says is downright candid and amazing to listen to.

The Startup Ponzi Scheme

To quote from Chamath:

“We’re in the middle of an enormous multivariate Ponzi scheme, let me explain that to you, because it’s important for you to understand.

You get courted by investors, these are not people writing cheques out of their balance sheet. They’re doing a job with other people’s money. And for that they get one thing that’s obvious which is a yearly fee. And then something that’s non-obvious which is a part of the gains if what you do works. That’s how a fund that invests in you works, that fund is getting paid fees every year and cary at the back end if it works.

They come to you, they’re like “We want to partner with you, you’re the best we’re going to help, you’re so awesome, have a fleece fest, it has your logo on it. We backed blah blah blah company”

That’s the basic pitch.

So you say yes! Then they’re going to give you a million bucks and then you go to your first board meeting.

“How fast are you growing” okay grow faster. Well, it would probably shock you to know that almost 40 cents of every venture dollar right now goes right back into the hands of Google, Facebook and Amazon.

What do you think that’s happening there, do you think that’s all profitable growth? No, that’s there to fund all of your superficial growth. Just because the VC gives you a million dollars and tells you to grow faster, do you have better product market fit in that moment?

No, you’re doing what you’re told to do which is to take their money and make the company grow. Superficially grow! Then what do they do? They turn around to their buddies and say “look at this thing it’s growing you should do the series B”. Then they come into a board meeting they’re like “guys, I think we should raise a B”

They’re like “Hey, you should raise a B” and some different firm, which they’re all buddies do the B, mark it up for 5x. Now what happens is fund A’s returns looks genius on paper.

Fund B comes into the board meeting now “hey how fast you’re growing? hmm… you gotta grow faster” now 40 cents of every dollar there goes into Facebook and Google and Amazon. You’re buying even more unprofitable growth, it’s not even clear whether those LTVs and those CACs make any sense.

It doesn’t matter, you’ve been told to grow. So you’re growing you’re doing your job. Did your product market fit actually change in that moment? Probably not, but you continue to pump money into those things. Then the series B investor says “hmm we should raise a Series C we’re running out of money” well, of course you are cause 40 cents of every dollar just went back into the hands of Facebook Google and Amazon.

They introduced it to another buddy, that buddy is like “yeah this looks great” boom! Fire the money in. Now A has an even better markup, B has a markup, C has a basis and is like “hey, how fast are you’re growing? maybe you should grow faster”

Now meanwhile somewhere between the B and the C round the guy who runs fund A is like “I should raise a second fund, I am pretty good at this” and goes to a bunch of investors and says “look at my IRR it’s amazing, isn’t this amazing” and the investors like “yeah this is amazing here, here’s more money” and then now he or she goes and finds another batch and starts the process.

Then somewhere between the C and the D the B guys are like “I’m pretty good at this, this is easier than I thought, I should raise a second fund! maybe I’ll make it a slightly bigger fund. I should be doing bigger checks” raises a B right raises fun 2. Finds fund A’s batch of second companies and says “hey let’s work together again we are good at this together” this is what’s happening now.

When you wake up every day and you read a newsletter and you notice that umpteen companies are getting funded for every single idea, and that the quantum of dollars are going up and that all of a sudden you’re reading about investors you’ve never ever heard of. That is what something like this looks like played out in real life.

You have the cream of the crop who will still do a good job, but who now have to raise larger and larger funds, they own less and less of the companies, the return not as good, and then you have everybody else who’s chasing chasing chasing and playing this sort of hot potato game hoping to raise a fund, and then a second fund and a third fund, and then the biggest thing happens.

That whole industry that theoretically services you guys are no longer about your success. Because your success is about their carry, and they couldn’t give a fuck. They care about the fees, it’s not very difficult to get out a Google spreadsheet and figure out, “at how many dollars, does 2% of those dollars divided by the five or six partners at that firm are greater than their share of profits for you it and some number of exits” and then you wonder why they’re more concerned about how much money you’re spending on Facebook Google and Amazon.

But think of how much money the fund would have to be, net of expenses for you to pay back it’s super complicated. My point is the incentives in this industry are the most out of whack they’ve ever been, it’s a bit of a charade.

Growing slow, growing profitable.

Chamath goes on in the discussion to talk about how giants like Amazon grew at 25% ARR for 25 years, great things aren’t really built over-night regardless of the hype.

We’ve taken a little bit of a different approach to how we invest in software. It’s not like we have a lot of things under our belt, combined the software products we’ve invested in (as concepts) just broke a 7 figure bottom line in ARR.

Our best success-story is the a homegrown product we’ve grown out over the years called Publisher Rocket. It’s the big fish in an absolutely tiny pond of self-published authors on Amazon.

But the beauty of it is that it’s a steady growing product that has a validated market fit, with tens of thousands of customers with healthy bottom lines.

This is the philosophy of the products that we’ve invested in (be-it technology or not) and the way we operate. It’s about delivering value not Hype. We’ll probably never back the next big unicorn, we’ll actively stay away from it. But you can make great contributions to the world and generate significant alpha without being the next Tinder for Human Centipedes.

Also, if you ever want to take the piss out of the cesspool that is the ecosystem, College Humor has a wonderful series of videos, they’re old but it’s honestly just fine art.

good read mate.

Spot on ⭐️

It’s true. Many people just look at the IRR, rather than the fundamental reason behind those IRRs.

Great read.

I couldn’t refrain from commenting. Exceptionally well

written!

Here is my website CBD oil for dogs